Přehled kategorií

- All

- Analysis (1)

- Building certification (3)

- Carbon footprint (3)

- Metering (1)

- Uncategorized (8)

O našem blogu

Přečtěte si, proč tento blog píšeme. Najdete zde také informace pro přispěvovatele.

EU Taxonomy: how it works and what it means for companies

The EU Taxonomy is a fundamental framework for directing investments towards sustainable activities and preventing greenwashing. This article explains how it works, its objectives, and what it means for companies in terms of alignment assessment and reporting requirements.

EU Taxonomy

This tool is becoming key in directing investments within the EU towards a carbon neutral future. Through standardizing sustainability criteria, it seeks to protect these definitions from greenwashing and to accelerate investment towards activities which are already sustainable or require transitional support.1

What is the EU Taxonomy?

The EU Taxonomy is a classification system, which was put into force on July 12 2020 as one of the many parts of the European Green Deal policy, aiming to achieve climate neutrality by the year 2050, in alignment with the goals set out by the Paris Agreement in 2016.2

As a classification system, the EU Taxonomy establishes criteria for determining whether an economic activity can be considered environmentally sustainable. It provides investors with a structured and transparent reference point for assessing alignment with a net-zero trajectory, while also supporting broader objectives beyond the environment.3

A User Guide to Navigate the EU Taxonomy for Sustainable Activities, provided by the European Commission, defines the main goals of this system as:

- Help scale up investments in projects which make a substantial contribution to at least one of the six objectives outlined by the EU Taxonomy, and therefore accelerate the implementation of the European Green Deal

- Protect investors from greenwashing4

- Help companies plan and finance their green transition.

- Help mitigate market fragmentation5 and information asymmetry

- Help shift investments to where they are most needed to meet the EU's climate and environmental ambitions.

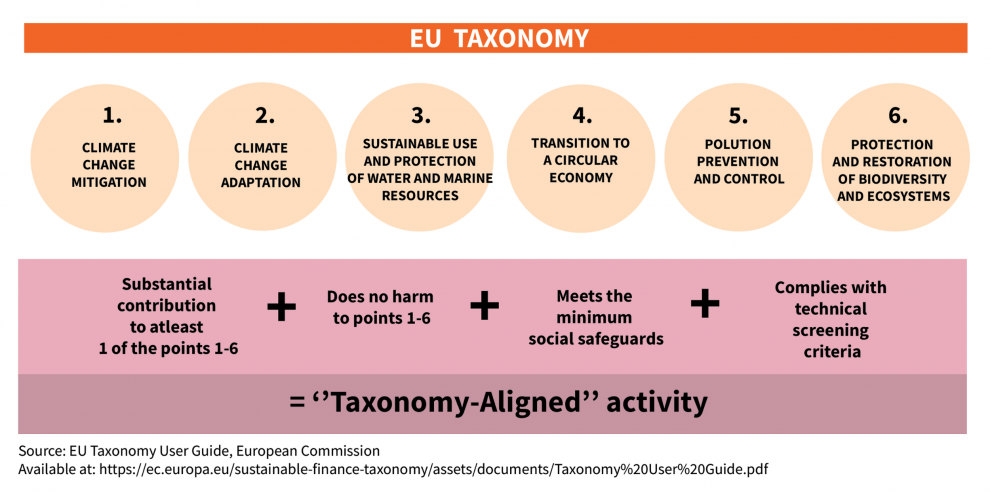

The six environmental objectives defined by the EU Taxonomy are:

- Climate change mitigation

- Climate change adaptation

- Sustainable use and protection of water and marine resources

- Transition to a circular economy

- Pollution prevention and control

- Protection and restoration of biodiversity and ecosystems6

Sustainable economic activity:

There are currently 4 criteria set out in the Taxonomy Regulation that must be met for an economic activity to be considered “Taxonomy-aligned” and therefore sustainable.

- making a substantial contribution to at least one of the six environmental objectives

- doing no significant harm to any of the other five environmental objectives - ''Do No Significant Harm'' (DNSH)

- complying with minimum safeguards

- complying with the technical screening criteria

In addition to economic activities which must, on their own majorly contribute to the main six objectives outlined by the taxonomy, a specific subtype of economic activities is recognized by the taxonomy as “enabling” activities. These activities may directly enable and support other activities contributing to the main six objectives outlined above, provided they:

do not result in undermining long-term environmental goals, considering their economic lifetime, and demonstrate a substantial positive environmental impact based on life-cycle considerations.

A type of activity defined as a “transitional” activity may apply to activities which significantly contribute to the environmental goal of climate change mitigation, but where no low-carbon alternatives are yet available. Although they are not low-carbon activities, they support the transition to a climate-neutral economy in line with the goals of the Paris Agreement.7

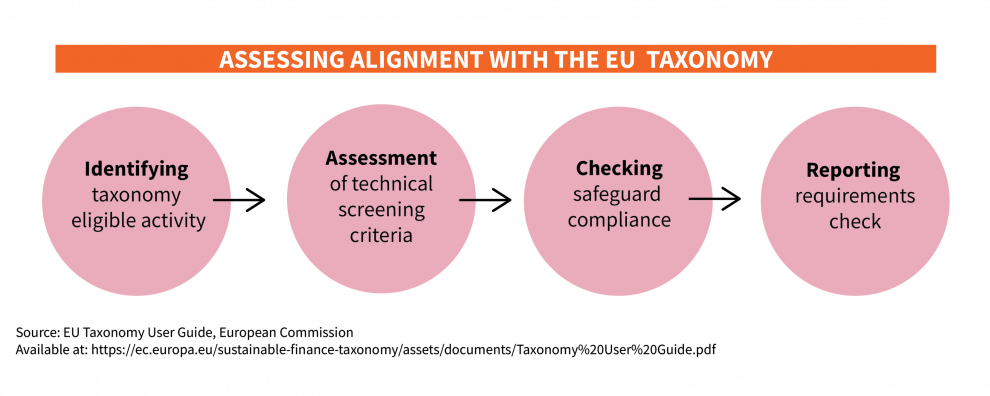

Assessing alignment with the EU Taxonomy:

Identification of activities eligible under the Taxonomy

To determine whether a company's economic activity can be considered “Taxonomy-aligned”, all economic activities of a company must be compared to activity descriptions outlined in the Climate Delegated Act and the Complementary Climate Delegated Act. These delegated acts define sector-specific activities that may potentially qualify as environmentally sustainable.

Currently the EU Taxonomy Navigator available from the European Commission's website serves as a useful visual representation of sectors, activities and criteria included in the EU Taxonomy delegated acts. Certain economic activities carried out by a company may not yet be included within the current scope of the Taxonomy. The absence of an activity from the existing list should not be interpreted as an indication of environmental unsustainability but may mean that the criteria have not yet been developed for these activities and are therefore not yet eligible under the EU Taxonomy.8

Assessment of technical screening criteria

After eligible economic activities have been identified within a company’s operations, a gap analysis is conducted to assess their current position against the Taxonomy’s technical screening criteria.9

This involves evaluating environmental performance and reporting practices, as well as identifying areas requiring improvement to achieve alignment. The assessment should also incorporate the Do No Significant Harm (DNSH) criteria to ensure that activities do not significantly undermine any of the other environmental objectives. The EU Taxonomy Regulation specifies a list of potential activity which is viewed as causing significant harm in relation to the six objectives.

Businesses must have reliable data collecting and monitoring systems in place to meet Taxonomy's disclosure obligations, such as compiling accurate data on energy consumption, greenhouse gas emissions, and other relevant environmental impacts.

The implementation of consistent and structured sustainability tracking systems enhances transparency in reporting and facilitates verification during audit processes.10

Assessment of compliance with minimum safeguards

An activity cannot be considered Taxonomy-aligned unless the undertaking respects pre-determined social and governance standards.

The Taxonomy Regulation requires companies to operate in line with internationally recognized frameworks, particularly the OECD Guidelines for Multinational Enterprises and the United Nations Guiding Principles on Business and Human Rights.11

Review of reporting requirements

Companies falling under NFRD/CSRD12 must disclose the share of environmentally sustainable economic activities that are aligned with the EU Taxonomy criteria.

The Disclosure Delegated Act specifies reporting requirements and defines key performance indicators (KPIs). For banks and insurance companies, a specific indicator – Green Asset Ratio (GAR) – is required. These institutions must disclose the share of their loans, advances, and securities financing Taxonomy-aligned activities.

Companies subject to sustainability reporting requirements must disclose Taxonomy alignment in their annual management report (or a dedicated sustainability section) in accordance with the Corporate Sustainability Reporting Directive. They must report the proportion of activities that are Taxonomy-eligible and Taxonomy-aligned, along with the methodology used. Compliance is demonstrated through regulated public reporting and verified through audits and supervisory oversight.13, 14

Conclusion

A company seeking to demonstrate compliance with the EU Taxonomy Regulation should primarily rely on EU legislation and implementation guidelines. The European Commission has created an online platform with tools that help users understand the EU Taxonomy and support its practical implementation and reporting requirements.

The EU Taxonomy Navigator

https://ec.europa.eu/sustainable-finance-taxonomy/

A User Guide to Navigate the EU Taxonomy for Sustainable Activities

https://ec.europa.eu/sustainable-finance-taxonomy/assets/documents/Taxonomy%20User%20Guide.pdf

1EU Taxonomy for sustainable activities, https://finance.ec/sustainable-finance/tools-and-standards/eu-taxonomy-sustainable-activities_en. 17 December 2025

2FAQ: What is the EU Taxonomy and how will it work in practice?, https://finance.ec/system/files/2021-04/sustainable-finance-taxonomy-faq_en.pdf. Accessed 20 Feb. 2026.

3European Commission, editor. A User Guide to Navigate the EU Taxonomy for Sustainable Activities. Publications Office, 2023.

4Greenwashing – Defined by the EU Taxonomy User Guide as: Sustainability claims that are exaggerated or not substantiated.

5Market Fragmentation – A market composed of multiple highly-incompatible technologies or technology stacks, forcing prospective buyers of a single product to commit to an entire product ecosystem, rather than maintaining free choice of complementary products and services.

6European Commission, editor. A User Guide to Navigate the EU Taxonomy for Sustainable Activities. Publications Office, 2023.

7European Commission, editor. A User Guide to Navigate the EU Taxonomy for Sustainable Activities. Publications Office, 2023.

8European Commission, editor. A User Guide to Navigate the EU Taxonomy for Sustainable Activities. Publications Office, 2023.

9FAQ: What is the EU Taxonomy and how will it work in practice?

"The technical screening criteria for ‘substantial contribution’ to an environmental objective ensure that the economic activity either has a substantial positive environmental impact or substantially reduces negative impacts on the environment, e.g. substantially reduced levels of greenhouse gas emissions. The technical screening criteria for ‘do no significant harm’ ensure that the economic activity does not impede on the other environmental objectives from being reached, i.e. it has no significant negative impact on them."

10Understanding The EU Taxonomy And Its Environmental Impact. https://www.otcflow.com/insights/understanding-the-eu-taxonomy. 4 October 2024

11European Commission, editor. A User Guide to Navigate the EU Taxonomy for Sustainable Activities. Publications Office, 2023.

12NFRD: Non-Financial Reporting Directive - Adopted in 2014, EU directive requiring certain large public-interest entities to disclose information on environmental, social, human rights, and anti-corruption matters. CSRD: Corporate Sustainability Reporting Directive - Adopted in 2023 replaces the NFRD and significantly expands sustainability reporting requirements, including broader company coverage, mandatory reporting standards, and external assurance.

13European Commission, editor. A User Guide to Navigate the EU Taxonomy for Sustainable Activities. Publications Office, 2023.

14European Union, DIRECTIVE 2014/95/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 22 October 2014 (2014)

- 27. březen, 2026

- By: Team Enerfis

- Category: Carbon footprint